(22)")

What Are Card-Linked Offers? How CLOs Work in Performance Marketing

Once a consumer activates an offer, the rest is effortless: they tap their Mastercard at the coffee shop and receive cashback automatically – no coupon code, app check-in, or barcode required at checkout. The reward just shows up. That frictionless experience is exactly why CLOs are becoming one of the most interesting channels in performance marketing.

If you’ve been spending all your budget on promo codes, paid social, and click-based campaigns, CLOs deserve a serious look. The card-linked offers platform market was valued at $9.4 billion in 2025 and is projected to reach $28.7 billion by 2034, growing at a compound annual rate of about 12.6%, according to a March 2026 Market Intelo report. That’s not a niche trend, it’s a real shift in how brands connect with buyers at the point of transaction.

What a card-linked offer actually is

A card-linked offer (CLO) is a promotion attached directly to a consumer’s debit or credit card through a bank, loyalty program, or rewards app. When the cardholder makes a qualifying purchase at a participating merchant, the reward is typically cashback, a statement credit, or bonus loyalty points that post automatically. No code to enter. No receipt to upload.

The mechanics go roughly like this:

- Link The consumer registers their card with a CLO program (a bank app, a loyalty platform, or a rewards app).

- Activate Some programs require the user to opt into specific offers; others enroll automatically.

- Shop The consumer pays normally at a participating merchant, in-store or online.

- Earn The payment network matches the transaction to the active offer and the reward posts, usually within a few days to a few weeks.

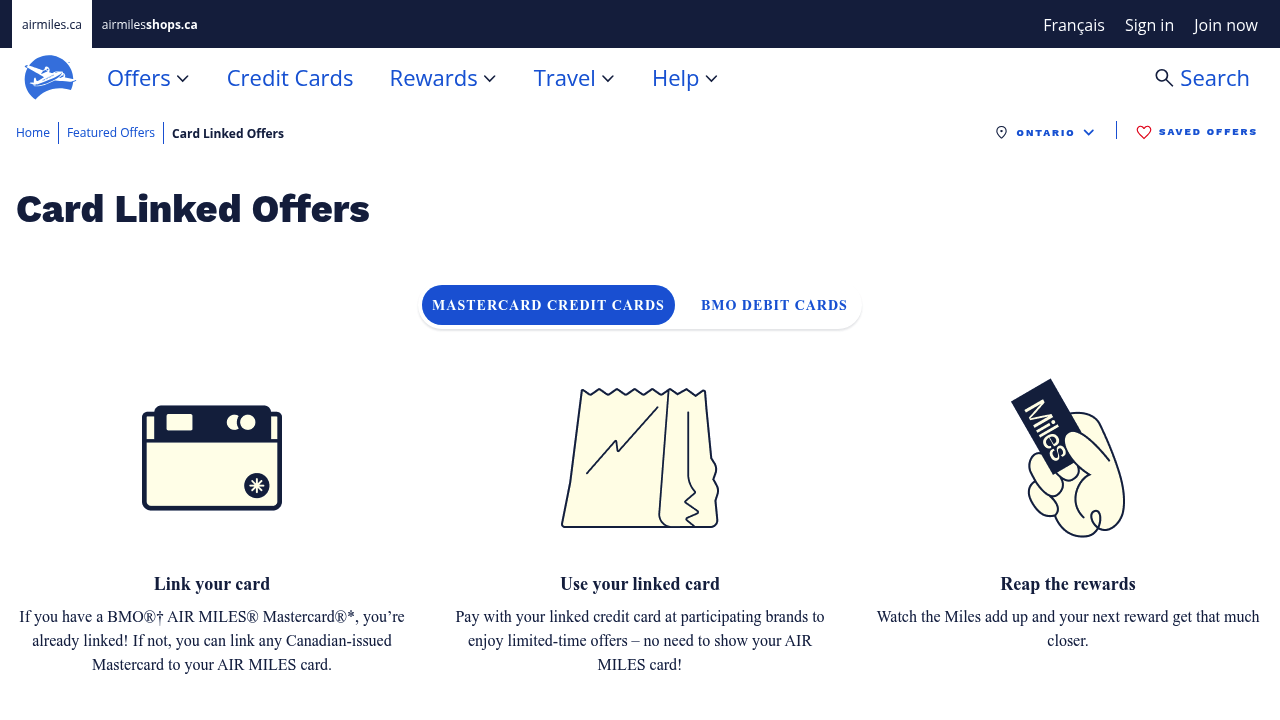

In Canada, AIR MILES Card Linked Offers is one of the clearest examples of this in action. Collectors link any Canadian-issued Mastercard to their AIR MILES account, shop at partner brands without scanning a loyalty card, and earn bonus Miles automatically. BMO cardholders are even enrolled automatically.

For brands, the interesting part isn’t the consumer experience alone it’s what sits underneath it: real, verified transaction data flowing through the payment network. That’s what makes CLOs such a different animal from most performance marketing strategies you’re currently running.

Source: Air Miles Website

How CLOs differ from promo codes and affiliate channels

Most performance marketers already run offers through affiliate programs, discount codes, and cashback portals. CLOs occupy a distinct lane that’s worth understanding on its own terms.

With a standard affiliate link or promo code, attribution happens at the click or the code entry. That works for e-commerce but falls apart the moment a consumer walks into a physical store. CLOs track the actual payment transaction, so attribution extends to offline and in-person purchases, a closed loop that click-based models simply can’t close.

Here’s a quick side-by-side:

The attribution advantage matters a lot for brands running CPA campaigns across multiple channels.

That said, CLOs aren’t a replacement for affiliate and promo-code strategies. They’re a compliment. Promo codes, for instance, still outperform for top-of-funnel new customer acquisition and influencer campaigns where the personal recommendation is part of the value. CLOs are powerful for both retention and acquisition: they can drive repeat purchases and basket size among existing customers, while also targeting new or lapsed shoppers with stronger incentives to support user acquisition.

The performance marketing case for CLOs

From an advertiser’s perspective, there are a few things that make CLOs genuinely compelling compared to other pay-for-performance models.

You only pay when a transaction happens. CLOs are typically structured on a pay-per-transaction basis. No impression costs, no cost-per-click bleed. This aligns directly with how most performance budgets are structured: you want to pay for outcomes, not reach.

Targeting runs on real spending behaviour. Bank-controlled transaction data is arguably the most accurate signal available to marketers. You can target consumers who have spent at a competitor, reach customers who haven’t visited in 90 days, or build look-alike audiences from your highest-value buyers. That’s targeting that cookie-based display advertising can’t replicate.

Closed-loop measurement is built in. When a consumer redeems a CLO, the merchant and platform know exactly what was purchased, at what value, and when. There’s no reliance on pixel firing or UTM parameters surviving across devices. A June 2024 R3 Marketing analysis found that integrating credit cards into loyalty programs delivered a 19% lift in overall performance scores and a 17% improvement in visit frequency, concrete evidence that transaction-linked rewards change purchase behaviour.

They stack with other channels. A consumer who receives a targeted CLO from their bank can also be reached through paid social or email. Brands running omni-channel strategies find that CLOs add an incremental conversion layer on top of existing campaigns, a particularly valuable quality for affiliate marketing management programs trying to squeeze more out of their publisher mix.

CLOs and the cookieless environment

If you’ve been keeping a close eye on the browser privacy landscape, CLOs start to look even more interesting. As noted in a September 2025 piece on Substack’s Affiliate for Publicists, CLOs are “inherently privacy-compliant and don’t rely on third-party cookies or device IDs.” The targeting signal is the payment card itself, a first-party relationship between the bank and the cardholder.

Google’s ongoing privacy sandbox changes mean marketers are under increasing pressure to find channels that don’t depend on cross-site tracking. CLOs sidestep this problem entirely. The offer is matched to the transaction at the bank level, which means it works regardless of what happens to cookies in Chrome, Safari, or Firefox.

For performance marketers building a digital advertising strategy that needs to hold up over the next few years, that’s a meaningful structural advantage. First-party data is only going to become more valuable, and CLOs are one of the cleanest first-party data channels that exist at scale.

What CLOs look like in practice for advertisers

A CLO partner with access to bank transaction data can identify that exact segment, serve them an offer through their banking app, and only charge you when they transact at your brand.

The typical CLO campaign flow for an advertiser:

- Define the target audience (new customers, lapsed buyers, competitor switchers)

- Set offer terms (e.g., 10% cashback on first purchase, minimum spend $50)

- The CLO platform distributes the offer to matching cardholders through bank apps, loyalty portals, and third-party rewards apps

- Consumers activate and shop normally

- Transactions are verified and commissions are paid on confirmed purchases

- Reporting shows incremental sales, redemption rate, and return on ad spend

The measurement is clean and the model is inherently brand-safe because the offer only activates on a real purchase there’s no incentive for fraudulent clicks or fake leads in the way that plagues some other performance channels.

For publishers and CLO partners, the model works similarly to CPA affiliate marketing. You earn a commission when a cardholder completes a qualifying transaction. The difference is that your “creative” is the offer in a bank’s app rather than a landing page, and the “conversion” is tracked by the payment network rather than a pixel. If you’re already familiar with what affiliate marketing is and how performance fees work, CLOs slot into that mental model without much translation.

Challenges worth knowing about

CLOs aren’t without real limitations, and glossing over them doesn’t help anyone make a good decision.

Consumer awareness is still low. Many cardholders don’t actively check their bank app for linked offers, which limits redemption rates unless the CLO platform has a strong activation mechanism push notifications, email, or prominent in-app placement.

The publisher ecosystem is more concentrated. Unlike affiliate networks where thousands of publishers can participate, CLO distribution runs through a smaller number of banking and fintech partners. Getting meaningful reach often means working with a large platform or accepting a narrower audience.

Attribution isn’t always real-time. Transaction matching can take days, which makes rapid campaign optimization harder compared to click-based channels where you see results in hours.

Minimum spends and offer terms require careful structuring. Poorly calibrated offer terms (too-low cashback, too-high minimum spend) result in low activation rates. There’s more friction in setting up a compelling CLO than simply publishing a coupon code. That said, brands can reduce this risk by starting with shorter 1-month pilot campaigns, measuring performance and incremental lift, and then recalibrating the offer structure based on real transaction data before scaling spend

None of these are fatal flaws they’re just operational realities that should factor into how you allocate your performance marketing budget.

Where CLOs fit in your performance mix

Card-linked offers often perform best as a retention and frequency driver, but they can also support customer acquisition when paired with the right targeting and offer structure. Think of them alongside your broader performance marketing mix: affiliates and paid search can drive new visitors through the door, while CLOs can both re-engage existing customers and introduce your brand to highly targeted, transaction-verified audiences through banking and rewards ecosystems.

Brands seeing the best results with CLOs tend to share a few traits: they have an established customer base worth activating, they sell in categories with repeat purchase behaviour (dining, grocery, fuel, retail), and they have some tolerance for the longer setup and validation cycle that CLO platforms require compared to a quick coupon drop.

For marketers already running data-driven campaigns, especially those managing omni-channel programs across financial affiliate programs, retail, and consumer services, CLOs add a credible, measurable layer that’s genuinely difficult to replicate with other tools.

As the channel matures and bank apps improve their user experiences, expect activation rates and advertiser adoption to climb. That’s hard to replicate with traditional paid media. This is why CLOs are getting serious attention from performance marketers.

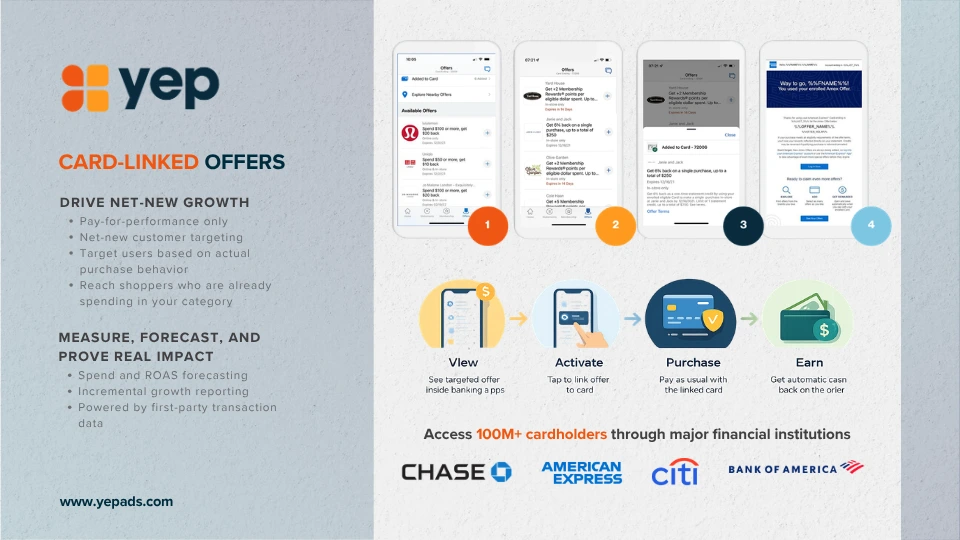

How Brands Are Using CLOs Through Yep Ads

At Yep Ads, we’re seeing growing interest from brands looking for more measurable, transaction-level performance channels – especially as attribution across traditional paid media becomes harder to track cleanly.

One of the biggest advantages of CLOs is that they combine premium placements with closed-loop measurement. Instead of paying for impressions or clicks, brands only pay when a verified purchase actually happens.

CLO Placements Across Banking & Rewards Ecosystems

Through our partnerships, brands can access CLO placements across major banking and rewards environments, reaching more than 100M+ cardholders through ecosystems tied to providers like Chase, American Express, Citi, Bank of America, and others.

These campaigns are structured around:

- pay-for-performance models

- transaction-level attribution

- cashback or statement-credit offers

- premium banking and loyalty placements

Typical campaigns include:

- percentage cashback offers

- fixed cashback incentives

- minimum-spend promotions

- seasonal or retention-focused campaigns

Because these programs run on verified transaction data, brands also gain access to:

- incremental lift reporting

- transaction-level reporting

- forecasting on expected spend and ROAS

- audience-level targeting opportunities

Заключительные размышления

CLOs won’t replace affiliate, paid social, or search. But for brands focused on measurable growth, repeat purchases, and privacy-safe targeting, they’re quickly becoming one of the most interesting channels in the performance mix.

Вам также может понравиться

- Brand Building vs. Short-Term Performance: Why the Smartest Brands Do Both

- Meta’s Andromeda Update: Facebook Algorithm Change

- What Is Brand Awareness? Why It Matters and How to Grow It

- LLM Advertising Wave: New Acquisition Channel

- Affiliate Marketing Compliance: What You Need to Know

Поделиться